In the second position, Ningbo-Zhoushan Port recorded 3.22 million TEUs of container throughput in June. For H1 2023, it accumulated a total of 17.68 million TEUs, experiencing a modest 1.2% year-on-year growth.

At the third spot, Shenzhen Port saw a June container throughput of 2.62 million TEUs. However, it faced a challenging H1 2023, with a total container throughput of 13.53 million TEUs, reflecting a 6.1% year-on-year decline. Notably, Shenzhen Port stands as the only port among the TOP15 container ports in the country to experience a year-on-year decline.

This decline in Shenzhen Port’s container throughput can be attributed to various factors. The pandemic prompted the exit of new players in the American line, and the three major shipping alliances withdrew a substantial amount of trans-Pacific capacity. Given Shenzhen Port’s significant role in deploying services along the

American line, the temporary suspension or cancellation of many Asia-North America routes contributed to the decline in container throughput in H1 2023.

Furthermore, when compared to southern ports, northern ports such as Yingkou Port, Dalian Port, Qingdao Port, Rizhao Port, and Yantai Port exhibited more remarkable growth rates, all maintaining double-digit increases.

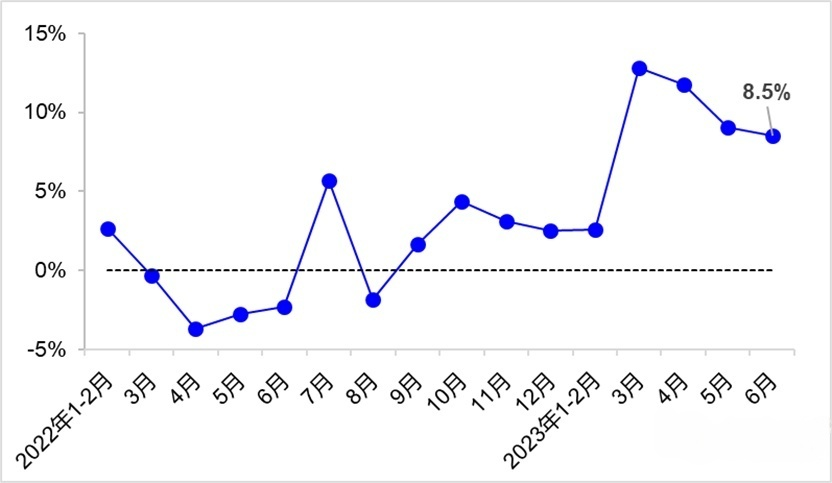

According to statistics from the General Administration of Customs, Sino-Russian trade recorded a total of $114.547 billion in the first half of 2023, marking an impressive 40.6% year-on-year growth. China’s exports to Russia alone reached $52.284 billion, indicating a remarkable 78.1% increase. This surge in Sino-Russian trade may serve as a significant driving force for the notable growth rates observed in northern ports.