In an intriguing twist amidst the announcements of FAK rate hikes on the Asia-Europe route by major players like Maersk, CMA CGM, and Hapag-Lloyd, MSC has taken an unconventional approach. Recent reports reveal that MSC, in a surprising move, has decided to slash FAK rates on the Asia-North Europe route. This reduction, amounting to approximately $200 per 40-foot container, has set the stage for a head-to-head pricing war with their collaborator in the 2M Alliance, Maersk.

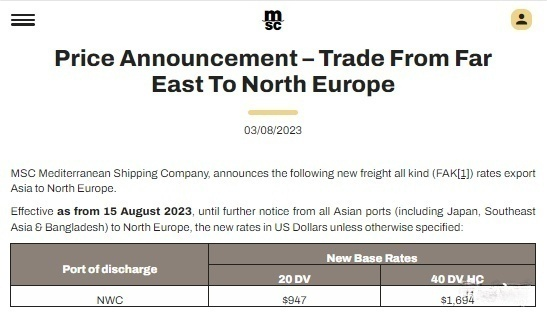

Effective from August 15th, MSC’s revised rates for the Asia-North Europe route are now set at $947 per 20-foot container and $1694 per 40-foot container. A marked contrast emerges when compared to Maersk’s earlier increase, which raised FAK rates to $1025 per 20-foot container and $1900 per 40-foot container, taking effect from July 31st.

Interestingly, this decision has sparked a ripple effect, as other prominent shipping companies are also considering rate adjustments for the Asia-Europe route. Notably, CMA CGM has revealed plans to raise their FAK rates to $1150 per 20-foot container and $2100 per 40-foot container from August 15th.

The backdrop to these shifts in rates is crucial, especially given last week’s unexpected cancellation of MSC’s independent “Swan” service on the Asia-North Europe trade lane. This cancellation hints at MSC’s strategic maneuvering to support its growth ambitions, possibly by leveraging competitive pricing, particularly for its independent services.

The backdrop of August 1st’s General Rate Increase (GRI) has added further intrigue. Initial post-GRI figures showcased a surge in spot container rates from Asia to Northern Europe. The Drewry World Container Index (WCI) climbed by a substantial 25%, settling at $1620 per 40-foot container. Similarly, the Shanghai Containerized Freight Index (SCFI) surged by a noteworthy $233 to reach $975/TEU, registering a remarkable growth rate of 31.40%. Meanwhile, the Ningbo Containerized Freight Index (NCFI) soared by an astounding 56.9% in a single week.

However, this upward trajectory was not sustained, as soft demand led to subsequent rate corrections. Notably, the latest NCFI for the Asia-North Europe route indicated a 7.8% dip in spot rates. NCFI’s commentary reflects this trend, highlighting, “The carriers’ significant unilateral rate hike last period was not supported by adequate market volume, leading to a pullback in rates this period.” Similarly, SCFI also declined by 2.87%, with concerns raised about the resilience of the European economic recovery.

As industry dynamics evolve, industry insiders are speculating on carriers’ pricing strategies. One NVOCC manager revealed that leading carriers might consider some flexibility in their minimum FAK rates. The absence of a conventional peak season this year might limit carriers’ ability to uphold GRI prices. Instead, carriers could aim to extract a reasonable share of profit from these pronounced rate hikes. The manager noted that a possible outcome could be alignment with MSC’s GRI, thereby putting pressure on Maersk to reconsider their pricing strategy and avoid relinquishing market share in the shared shipping segment.

This unfolding narrative is also influencing customer preferences. A thought-provoking question arises: “When you can secure more economical rates from MSC on the same vessel, why opt for Maersk?”

In a seemingly counterintuitive stance, Maersk’s CEO, Vincent Clerc, articulated during the Q2 earnings call that the liner division’s primary goal isn’t market share. Despite Maersk witnessing a 6.1% decline in container transport volume in Q2 compared to the previous year, its rival, CMA CGM, managed to achieve growth that exceeded industry averages.

Clerc emphasized that growth driven by low-profit margins holds limited value. He asserted, “We need to genuinely consider whether market share or profitability takes precedence. My wording may indicate a leaning towards prioritizing profitability over market share.”

With contrasting approaches emerging, it’s notable that MSC recently joined the SEA-LNG alliance, advocating for cross-industry cooperation and fossil-based liquefied natural gas as a transitional fuel towards achieving net-zero emissions. In contrast, Maersk’s decision to reject this strategy has amplified the disparities between these two influential maritime players.